1. A customer with a margin account believes the market is going to head lower and wants trade stock and options. Because of the bear market, put premiums have become very expensive and call premiums have declined. Stock XYZ is currently trading at $50, and the Aug 50 Calls are trading at $5 and Aug 50 Puts are trading at $15. In order to place this trade with the smallest capital commitment, what should the trader do?

Buy long 100 shares of XYZ at $50 and buy 1 XYZ Aug 50 Call

Buy long 100 shares of XYZ at $50 and sell 1 XYZ Aug 50 Call

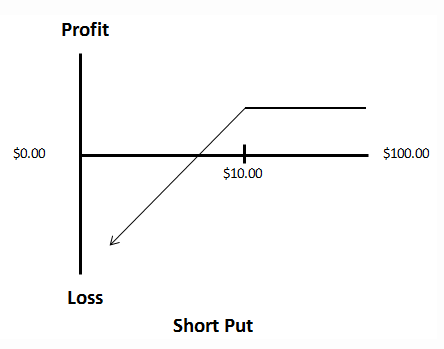

Sell short 100 shares of XYZ at $50 and sell 1 XYZ Aug 50 Put

Sell short 100 shares of XYZ at $50 and buy 1 XYZ Aug 50 Call

Answer: C

This trade is the best way to speculate on the market decline with the smallest capital commitment.

If the trader buys the put, they must pay a premium of $1500. And if the trader shorts the stock at $50, a 50% margin requirement is needed. This means $2500 will have to be deposited into the account to trade the stock short.

When a trader places a covered put trade, the $2500 on the short stock will be offset with premium collected from the short put of $1500. The net deposit for this position will be $1000. This is the smallest capital commitment for the trader.

2. A customer buys 200 shares of GE at 10 and sells 2 GE Jun 8 calls at $5. What is the maximum potential gain?

500

600

700

800

Answer: B

Stock delivered at $8 for exercised calls on stock that cost $10. This is a loss of $2 per share. $5 was collected in premiums from sale of Jun 8 calls, the net gain, if exercised, is $3.00, or $300 per contract x 2 contracts = $600

3. What can be used to efficiently hedge a broadly diversified stock portfolio?

Foreign exchange

Bonds

Precious Metals

SP500 Options

Answer : D

4. What is the best option position to hedge a short stock position?

Long Puts

Short Puts

Long Calls

Short Calls

5. A trader buys 100 shares of XYZ at $50 and buys 1 XYZ Jan 50 Put at $5. This position results in a profit when the price of ABC:

Goes above 30

Goes below 50

Goes above 55

Goes above below 20

Answer B

The trader paid $50 for the stock and $5 for the put, a total of $55 paid. If the stock moves to $55, that is the breakeven on the position. If the stock moves below $55, the trader can lose money because of the premium paid on the puts. The max loss is $5 because the trader can exercise the $50 put to limit losses on stock purchased at $55.

6. Intrinsic value is…

The difference between the strike price and market price of the underlying stock

The difference between the option price and the market price of the underlying stock

The strike price plus underlying stock price divided by 2.

The strike price minus market price plus premium paid

Answer: A

7. A trader owns 100 shares of XYZ stock and 1 XYZ put option. The customer wishes to sell stock by exercising the put but wants to keep the cash dividend. In order to receive the dividend, the trader cannot exercise the option:

Before the ex date

After the ex date

After the dividends are paid

Before the announcement date

Answer : A

8. In November a customer buys 1 XYZ Jan 100 Call @ $10 when the market price is $101. If the customer closes out the position prior to expiration by selling the call at $8, the gain or loss is?

$100

$200

$300

$400

Answer : B

9. A customer sells short 100 shares of ABC at $50 and purchases 1 ABC Jan 45 Call at $2.50. ABC drops to $40 and the customer closes the options contract at $1.50 and buys the stock at the current price. The customer has a profit or loss of…

500

700

900

1000

Answer : C

10. A trader sells 1 AAPL Jan 250 Call at $10 when the market price of AAPL is $240. What is the maximum profit potential of this position?

1000

1500

500

250

Answer : A

The maximum profit potential when selling a naked call option is the premium received. This occurs when the market drops and the call expires out-of-the-money.

11. A trader buys 100 shares of AAPL stock at $250 and buys 1 AAPL Dec 245 Put at $10.50 on the same day. The maximum potential gain is…

1050

Breakeven

Unlimited

0

Answer: C

The Put is brought against the stock as a hedge. If the market falls below 245, the put will be exercised and the stock will be sold at 245. However, if the stock was to continue to rise, the put would expire with no value, and the profit potential on the stock would be unlimited.

12. A trader is looking to enter a trade on stock ABC that is currently trading at $100. The order that was placed with his broker was 1 ABC Jan 100 Call and Short 1 ABC Jan 105 Call. This position is considered?

A Bear Put Spread

A Bull Put Spread

A Bear Call Spread

A Bull Call Spread

Answer : D

This trade is considered to be a Bull Call Spread and is used when the market outlook is bullish on a stock.

13. What of the following trades can be used to hedge a short position of 300 shares of AAPL stock?

1 x ATM Long Put

1 x OTM Long Call

3 x ATM Long Call

3 x OTM Long Put

Answer: C

Typically when option traders are looking for a hedge against their position, they will want to purchase at-the-money option contracts. Since the trader has 300 shares of the stock, this means they are required to purchase 3 options contracts. And to offset the negative direction on the short stock, they will need to cover this using a Call Option.

14. A trader buys 100 shares of AAPL that are trading at $200. A month later the stock increases to $225. The trader believes that the market will stay near this price and decides to sell 1 AAPL Jun 225 Call @ $15.00. AAPL then goes to $185 and the call options expire and the stock is liquidated at current market price. What is the total overall profit or loss on this trade?

No gain or loss

1500 loss

2500 gain

3000 gain

Answer: A

There is no gain or loss on this trade. Since the stock was purchased at $200, and the call option was sold for $15, that means the traders breakeven was $185. Since the stock was sold at $185, the trader did not make or lose any money on this position.